Limited Attention and Asset Price Efficiency: Evidence from NYSE Opening and Closing Ceremonies

- Click to get the pdf.

- Steve Crawford, Wesley Gray (me!), and Shastri Sandy

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our free Academic Alpha Database!

Abstract:

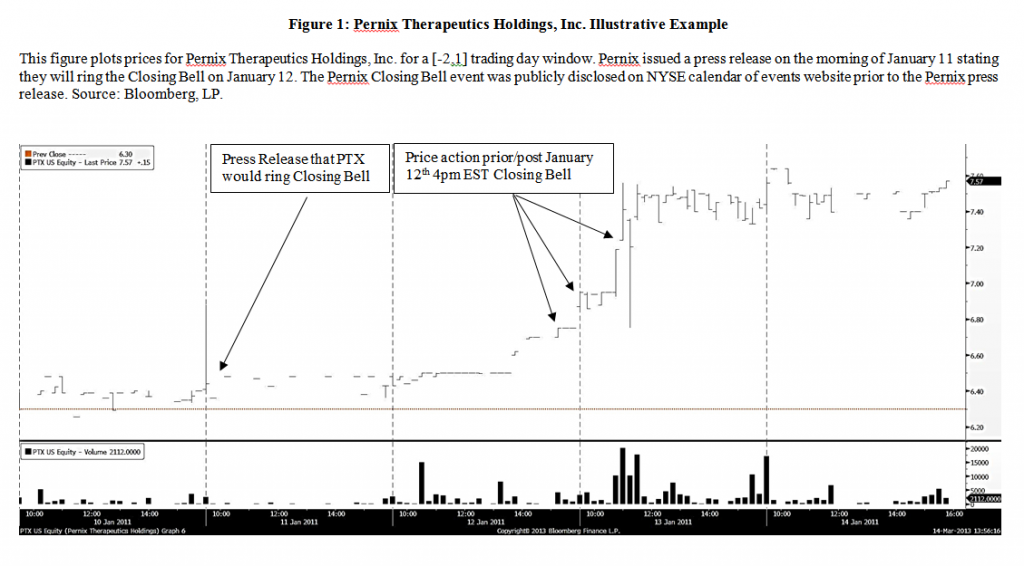

The limited attention hypothesis suggests that investors’ limited cognitive resources affect securities markets. We explore predictions from the limited attention hypothesis in the context of firms participating in NYSE’s Opening and Closing Bell ceremonies. In contrast to prior research, our unique experimental design allows us to more easily differentiate information shocks from attention shocks. We have two new findings: 1) Institutional investors are affected by limited attention and 2) limited attention has little influence on asset prices.

Data Sources:

NYSE, CRSP/COMPUSTAT, SEC

Alpha Highlight:

[Click to enlarge] The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Strategy Summary:

This is a paper I have been working on recently. My original hope was that the anecdote above was more systematic–it would be great to systematically earn a few percentage points trading around Bell events. Unfortunately, the plural of anecdote is data, and the data have spoken: the market is very efficient. There might be small trading opportunities associated with Opening Bell events (32bps in abnormal return after the Bell), firms with no previous Bell appearence (22bps), firms with no analyst following (25bps), or for firms that simply celebrate their listing (72bps in abnormal return). All in all, there is a lot more evidence that traders like to churn stocks when they are highlighted at a Bell Ceremony, but there is little evidence that the “smart money” allows prices to drift too far from fundamentals before trading against investors with limited attention.

If you’ve got interesting datasets or concepts you want us to test out, please send them along.

Thoughts on the paper? Or any experiences trading NYSE Bell stocks?

Would love to hear from traders…

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.